The Standard Group Plc is a

multi-media organization with investments in media platforms spanning newspaper

print operations, television, radio broadcasting, digital and online services. The

Standard Group is recognized as a leading multi-media house in Kenya with a key

influence in matters of national and international interest.

President William Ruto’s top two moneymen are this week making key appearances on the international stage, presenting themselves with the biggest opportunity for global economic leaders and investors to gain valuable clues on where they aim to steer policy.

Ruto's economic team is facing its first major international test this week at the annual meetings of the International Monetary Fund (IMF) and World Bank Group being held in the United States capital Washington D.C., amidst domestic economic challenges and recent public protests against proposed tax measures.

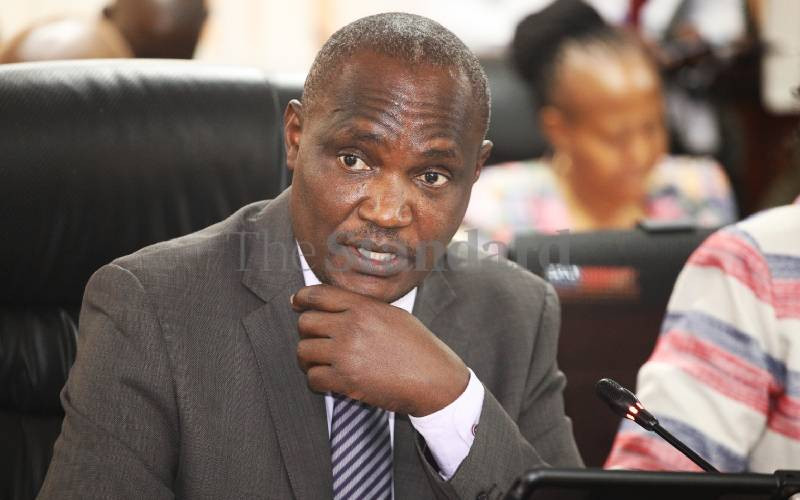

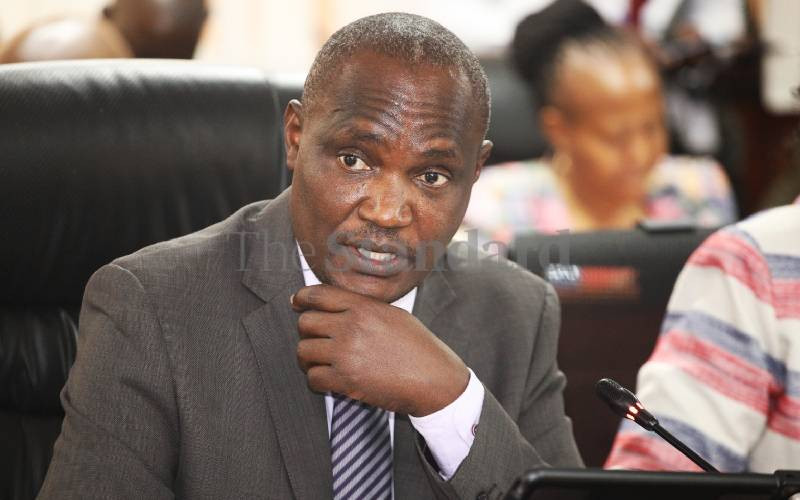

Treasury Cabinet Secretary John Mbadi and Central Bank of Kenya Governor Kamau Thugge are representing Kenya at these crucial forums. Mbadi, in particular, is on his first major overseas trip since his recent appointment.

The meetings come as the Ruto administration grapples with a significant fiscal hurdle.

The IMF this week reiterated calls for "sound macroeconomic fundamentals" and new tax policies to unlock billions in loans. This follows the rejection of a controversial tax bill by Kenyans, leaving a funding gap.

A crucial IMF executive board meeting later this week will determine the fate of Kenya's loan disbursement.

While the September visit of an IMF team led by Haimanot Teferra concluded with "productive discussions," no immediate financial assistance was announced. The IMF reiterated the need for new policies before any future funding.

The IMF's insistence on new taxes is particularly sensitive after widespread protests led by Gen Z activists erupted against IMF-backed tax measures. These protests, which resulted in tragic violence, exposed deep frustrations.

In response, President Ruto appointed Mbadi as the new finance minister, signalling a potential shift in fiscal strategy.

Mbadi's challenge is to balance public sentiment with meeting IMF expectations at a time when Kenya's economic outlook remains challenging, experts say.

The economy is slowing down, with sectors like construction and mining contracting. The Kenya Revenue Authority (KRA) is struggling to meet revenue targets, and the private sector is freezing hiring.

Mbadi had proposed reducing VAT, corporation tax, and PAYE rates as part of a medium-term revenue strategy. While this resonates with Kenyans burdened by rising costs, experts warn it could strain government finances.

National Treasury and Economic Planning CS, John Mbadi, PS Dr. Chris Kiptoo, and Central Bank Governor Dr. Kamau Thugge engaged in critical discussions during World Bank Group (WBG) and International Monetary Fund (IMF) Annual Meetings in Washington DC. [@KeTreasury, X]

The IMF meetings and ongoing discussions could be a turning point for Kenya's economic recovery. Mbadi's ability to engage the IMF and address public concerns will determine if Kenya can secure funding and build a more inclusive economy.

Mbadi on Monday met a top IMF representative who insisted that Kenya must put in place “sound macroeconomic fundamentals” to encounter growth.

“I met with Kenya's Minister of Finance John Mbadi and Central Bank Governor Kamau Thugge to discuss how the IMF can support Kenya’s efforts to establish sound macroeconomic fundamentals,” said IMF first deputy managing director Gita Gopinath.

“These are key to ensuring inclusive growth and creating much-needed jobs for Kenya’s youth.”

The Bretton Woods meetings come at a time when the newly reorganized Ruto government faces a fresh fiscal test after the IMF called on the Kenya Kwanza administration to develop new tax policies to unlock billions in loans.

During its recent visit, an IMF high-level team, led by Haimanot Teferra, concluded a critical visit to Nairobi from September 11 to 16, emphasising the urgent need for new policies amid the country’s evolving economic and fiscal challenges.

Despite the IMF team’s constructive discussions, no new funding was announced following the Nairobi meeting.

Instead, the IMF reiterated its commitment to supporting Kenya in identifying and implementing effective policy reforms.

The lack of immediate financial assistance underscores the IMF's stance that new policies are a prerequisite for any future funding.

The government must now navigate not only the technical aspects of tax reform but also the political ramifications of their decisions, especially in light of recent protests and loss of life.

The fresh calls by the IMF come in the wake of recent turmoil, including widespread protests led by Gen Z activists against IMF-backed tax measures that resulted in tragic violence, with dozens reportedly killed.

The rejected Ruto bill aimed at increasing taxes to meet IMF conditions but faced fierce opposition from Kenyans already burdened by economic hardships.

The protests, which erupted in response, revealed deep-seated frustrations among young Kenyans, exacerbating an already volatile situation.

This is a fresh test for President Ruto, who has faced mounting pressure to deliver on economic promises amid rising discontent.

When President William Ruto held a meeting with the IMF Managing Director Kristalina Georgieva on the sidelines of COP27 in Sharma El-Sheikh, Egypt. [PCS]

At the height of the Gen Z protests Mr Ruto was on the spot for seeking credibility abroad, even as discontent simmered at home over the slew of taxes.

The IMF recently also revealed this that it has encouraged Kenyan authorities to initiate governance diagnostics, a process aimed at identifying areas for improvement in governance practices.

"While governance reforms can take time, promoting good governance is essential to our engagement with Kenyan authorities," Ms Julie Kozack, Director of the Communications Department, IMF said.

Mr Mbadi announced plans to cut the value-added tax (VAT) from 16 per cent to 14 per cent, decrease corporation tax from 30 per cent to 25 per cent, and lower pay-as-you-earn (PAYE) rates, although specifics on PAYE reductions have yet to be detailed.

This proposal is part of the Treasury’s medium-term revenue strategy, which aims to improve tax administration, enhance compliance, and broaden the tax base.

“I will surprise you; in the medium term, we want to reduce tax rates. We are not looking at increasing taxes,” Mbadi declared.

While this plan has resonated with Kenyans burdened by rising costs of living, experts said it places Mbadi in a challenging position.

The new tax strategy could be a significant test for him, as it must balance immediate economic relief with the long-term sustainability of government finances, they said.

Experts argue that lowering taxes could stimulate economic growth and encourage compliance among taxpayers feeling the strain.

However, Kenya is currently navigating an IMF programme designed to stabilize its economy and address soaring public debt.

The IMF stresses the importance of fiscal discipline and revenue generation to ensure economic stability.

Analysts warn that the proposed tax reductions could threaten the government's ability to generate sufficient funds to meet its debt obligations.

The coming weeks will reveal whether Mr Mbadi can effectively engage with both the IMF and taxpayers to forge a path forward that addresses the urgent need for reform while fostering a more inclusive economy, experts said.

The Standard Group Plc is a

multi-media organization with investments in media platforms spanning newspaper

print operations, television, radio broadcasting, digital and online services. The

Standard Group is recognized as a leading multi-media house in Kenya with a key

influence in matters of national and international interest.

The Standard Group Plc is a

multi-media organization with investments in media platforms spanning newspaper

print operations, television, radio broadcasting, digital and online services. The

Standard Group is recognized as a leading multi-media house in Kenya with a key

influence in matters of national and international interest.