The Standard Group Plc is a

multi-media organization with investments in media platforms spanning newspaper

print operations, television, radio broadcasting, digital and online services. The

Standard Group is recognized as a leading multi-media house in Kenya with a key

influence in matters of national and international interest.

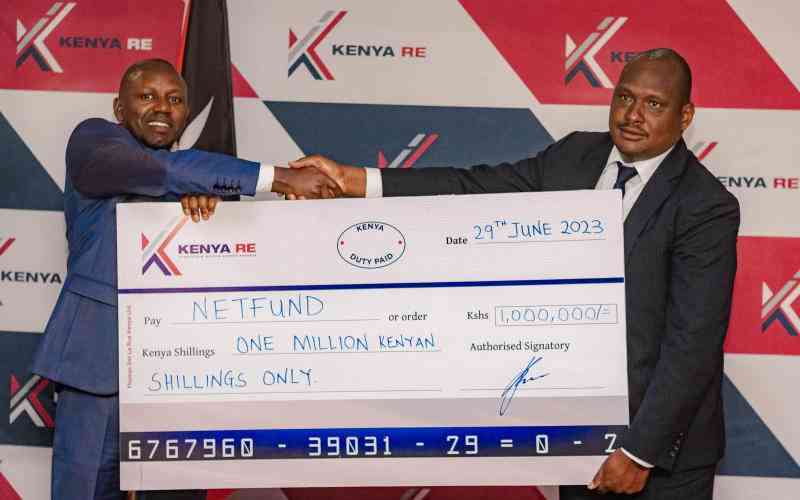

When Kenya Re Managing Director Hillary Wachinga handed over a cheque of One Million shillings to The National Environment Trust Fund (NETFUND) Chief Executive Officer. Samson Toniok on June 29, 2023 at Reinsurance Plaza, Nairobi. [Wilberforce Okwiri, Standard]

Get Full Access for Ksh299/Week.

Fact‑first reporting that puts you at the heart of the newsroom. Subscribe for full access.