×

The Standard e-Paper

Smart Minds Choose Us

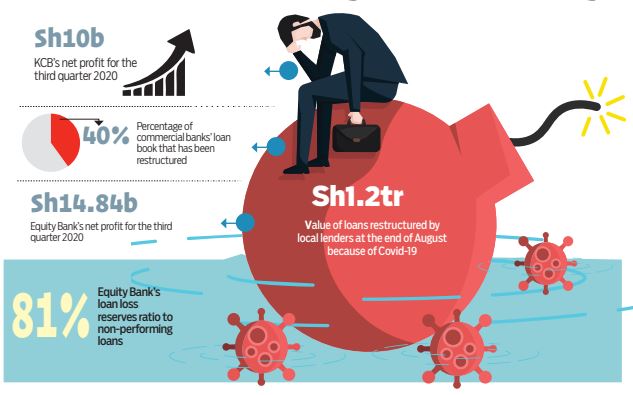

For six months, Kenyan banks have been like Atlas- the god in Greek mythology who carried the world on his shoulders.

Subscribe to our newsletter and stay updated on the latest developments and special offers!