×

The Standard e-Paper

Stay Informed, Even Offline

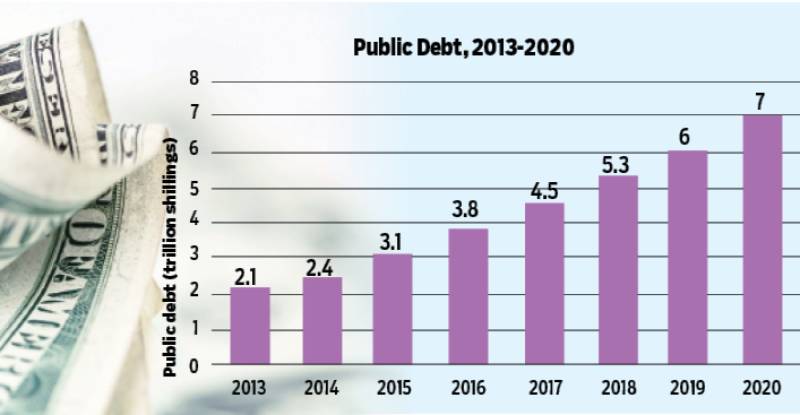

Kenya borrowed Sh374 billion in two months, pushing the country’s total public debt to more than Sh7 trillion by the end of August 2020.

Subscribe to our newsletter and stay updated on the latest developments and special offers!