×

The Standard e-Paper

Smart Minds Choose Us

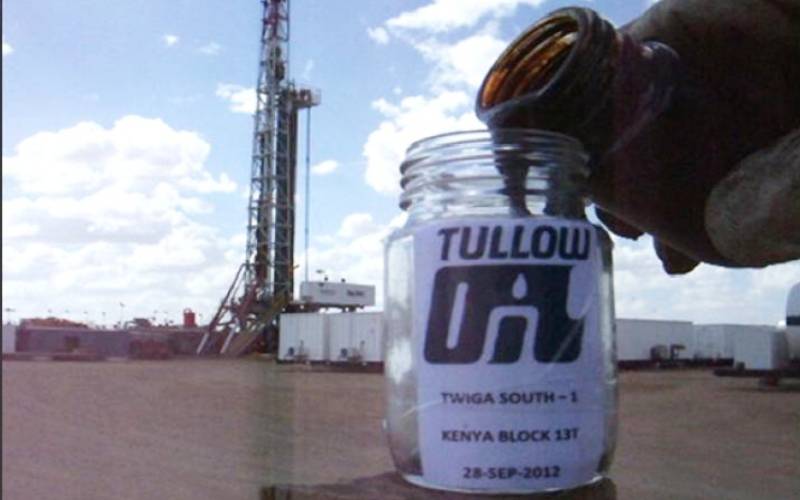

Perhaps Tullow Oil Plc, the company at the heart of Kenya’s much-hyped oil fortune, is a fraud.

Subscribe to our newsletter and stay updated on the latest developments and special offers!